KPIs That Actually Matter

A Modern Performance Framework for Scalable, Investable Restaurant Brands

By Robert Ancill

The Next Idea – Restaurant Consultants (TNI)

Why Restaurants No Longer Fail Quietly

Why Restaurants No Longer Fail Quietly

Restaurants don’t collapse overnight anymore. They erode. Margins thin. Labor churns. Guests still come, but they spend less, complain more, forgive less, and quietly disengage. By the time the P&L reflects the damage, the brand is already behind the curve.

For investors, franchisors, and multi-site operators, this presents a clear truth:

The greatest risk in hospitality is not cost, it is delayed awareness.

Key Performance Indicators (KPIs), when used properly, are not reporting tools. They are early-warning systems. But only if they evolve beyond basic cost control and start measuring guest tolerance, relevance, and future readiness.

This article outlines a modern KPI framework produced by The Next Idea (TNI) to help restaurant brands scale profitably, protect relevance, and make decisions with confidence.

The KPI Problem No One Talks About

The KPI Problem No One Talks About

Most restaurant groups already track KPIs. The problem isn’t absence of data, it’s misplaced focus.

Traditional KPIs answer questions like:

- Are Labor costs under control?

- Is food cost on target?

- Are sales up or down?

Modern operators need answers to far more dangerous questions:

- How much price pressure will guests tolerate beforedemand drops?

- Are we still culturally relevant to our core audience?

- Which parts of the experience are silently eroding loyalty?

- Is growth masking structural weakness?

At TNI, we see the same pattern repeatedly:

Operators manage efficiency. Investors need predictability. Franchisors need repeatability.

KPIs must serve all three.

The Four Pillars of Modern Restaurant Performance

TNI structures KPIs across four interconnected pillars:

People – Labor, leadership, and culture stability

Product – Menu, margin, and kitchen discipline

Place – Flow, conversion, and revenue efficiency

Perception – Guest tolerance, brand relevance, and trend alignment

Together, these pillars move KPIs from historical reporting to strategic foresight.

1. PEOPLE PERFORMANCE

Labor as a Value Engine, Not Just a Cost Line

Labor remains the largest controllable expense in hospitality, but also the most misunderstood. Investors often focus on wage percentages without recognizing that instability is more expensive than pay rates.

Core KPIs

- Wage Cost %

- Total Labor Cost % (true Labor cost)

- Labor Hours vs Sales

- Staff Turnover Rate

- Average Employment Tenure

- Sick Leave Incidence

- Average Hourly Rate

Segment Benchmarks (Indicative)

| Segment | Wage Cost % | Total Labor % | Annual Turnover |

| QSR | 22–28% | 25–32% | 80–120% |

| Casual Dining | 28–35% | 32–40% | 60–90% |

| Premium | 35–45% | 40–55% | 40–70% |

Investor Insight:

High turnover is not a labor problem, it is a systems and leadership risk that erodes consistency, brand trust, and unit economics.

2. PRODUCT PERFORMANCE

Margin Is Designed, Not Negotiated

Menu profitability does not happen by accident. It is the result of disciplined inventory management, menu engineering, and variance control.

Many concepts fail while “busy” because sales volume masks margin leakage.

Core KPIs

- Cost of Goods Sold (COGS %)

- Theoretical vs Actual COGS Variance

- Food Cost per Guest

- Menu Contribution Margin

- Kitchen Labor % (against food sales only)

- Stock on Hand (Days)

Segment Benchmarks (Indicative)

| Segment | Food COGS % | Beverage GP % | Stock Holding |

| QSR | 25–30% | 65–75% | 3–5 days |

| Casual Dining | 28–33% | 68–78% | 5–7 days |

| Premium | 30–38% | 70–82% | 7–10 days |

Investor Insight:

Popularity is not profitability. The most dangerous menu items are best-sellers with poor contribution margins.

3. PLACE PERFORMANCE

3. PLACE PERFORMANCE

Revenue Is a Function of Flow

Revenue growth is rarely limited by demand alone. It is constrained by:

- Seating efficiency

- Table turn times

- Attachment rates

- Conversion leakage

This is where strong concepts outperform average ones, even in the same location.

Core KPIs

- Average Spend per Head (ASPH)

- Covers & Repeat Visitation

- Sales Mix per Head

- Seating Efficiency

- RevPASH (Revenue per Available Seat Hour)

- Bounce Rate

- Basket Analysis

Segment Benchmarks (Indicative)

| Segment | ASPH (Relative) | RevPASH Focus |

| QSR | Low–Mid | Throughput |

| Casual Dining | Mid | Turn + Attach |

| Premium | High | Yield per Seat |

Investor Insight:

RevPASH exposes whether growth is driven by pricing power, flow discipline, or operational luck.

4. PERCEPTION PERFORMANCE

The KPIs That Predict Decline, or Defend Value

This is where most restaurant groups under-measure, and over-estimate safety.

TNI Customer Tolerance Index (CTI)

CTI measures how much operational or pricing friction guests will tolerate before reducing frequency, spend, or advocacy.

It assesses tolerance for:

- Price increases

- Waiting times

- Reduced service levels

- Menu simplification

- Experience inconsistencies

Why it matters:

Two brands can raise prices. Only one retains demand. CTI explains why.

TNI Trend Mapping Score

Trend Mapping tracks how well a concept aligns with:

- Current consumer behavior

- Cultural and generational shifts

- Competitive movement

This is not about chasing trends. It is about avoiding irrelevance.

TNI Trend Audit Rating

A structured audit assessing:

- Concept freshness

- Menu relevance

- Brand clarity

- Market differentiation

Investor Insight:

Most restaurant failures are relevance failures, not operational ones.

KPI TRUTH FOR INVESTORS & FRANCHISORS

KPIs do not create value.

Early decisions do.

The role of KPIs is to:

- Reduce blind spots

- Improve forecast accuracy

- Protect brand equity

- Enable scalable replication

At TNI, KPIs are not dashboards. They are risk-management tools for growth capital.

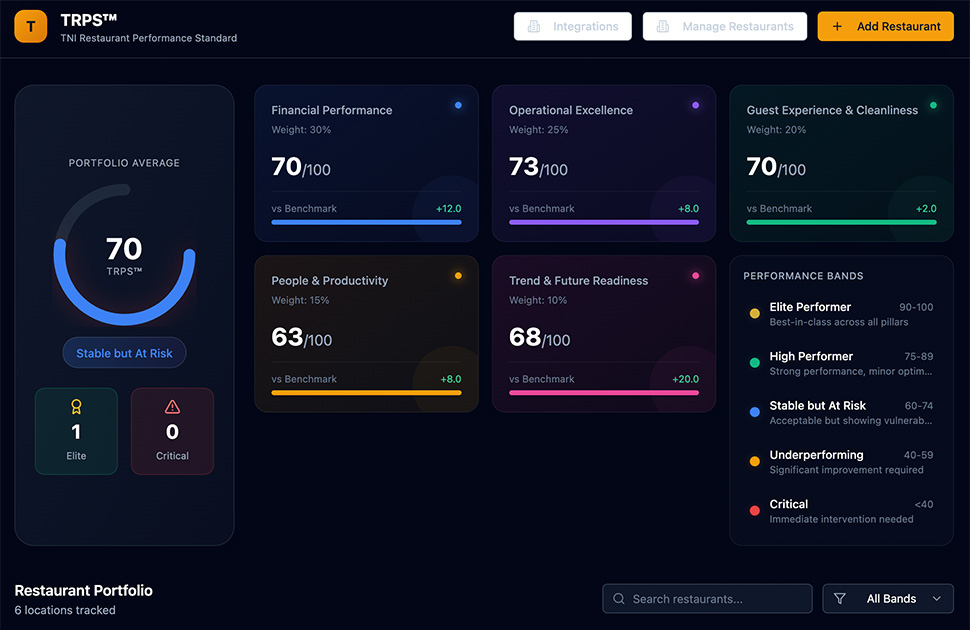

THE TNI KPI DASHBOARD (EXECUTIVE VIEW)

Weekly:

Labor %, COGS %, RevPASH, Sales Mix

Monthly:

Variance analysis, staff turnover, ASPH, CTI movement

Quarterly:

Trend Mapping Score, Trend Audit Rating, Brand relevance review

Final Thought

Final Thought

The restaurants that survive the next decade will not be the cheapest, the busiest, or the loudest. They will be the ones that measure what matters before it becomes obvious. That is the difference between operating restaurants, and building investable brands.